Preparing for Storm Season Part 1: Setting Up with Roofr

Join Pete McKendrick and Nic for an in-depth discussion on preparing for storm season with Roofr.

This episode of the Roofr Masterclass dives into crucial topics such as understanding the early onset of storm season, the importance of having a versatile product, and how to leverage various tools and workflows for optimizing insurance and retail roofing processes.

Learn about the Good Faith Estimate law, how to efficiently create detailed proposals, the importance of quick lead responses, and the use of checklists and automated tasks to stay organized and compliant. Don't miss this insightful session packed with tips and strategies to make the most of storm season!

All right. Good evening and welcome back everybody to the Roofer Masterclass. I am your host Pete McKendrick with my co host Nick and uh, excited to be here today. Uh, with this topic, you know, obviously timely it is the start, or I guess we're in the midst of, right? It's not really. Kind of like in the middle of it already, right?

We got early starts to it and then it's been a lull right now. So yeah. So the start of storm season here and, um, you know, obviously what we've built here at Roofer is a fairly versatile product. And so we're excited to share a little bit with you guys today about how we can help out, uh, to better prepare you for storm season.

So I think we have a two part series on this one. Don't we? We do. Yeah. So, so we'll be talking a little bit about some stuff today and then, uh, be sure to, if you are with us today, to be sure to join us on the next one as well. So, uh, you know, cause we can dive in a little deeper, but, uh, storm season. Yeah.

Early start. I don't remember there being storms quite so early as, uh, this year. No, it was, it came pretty quick. It was two back to back. Right. And then we even had like a cat. I don't know if it got up to the cat first. Five, but the one that just skirted up the Atlantic there. So there's some big ones and there's even a couple in the Pacific, but we haven't had any really make massive landfall except for the two there.

But I'm looking at the map right now, Pete, and there's a couple brewing in the, uh, in the Atlantic right now, three to be exact. So we'll see what happens. There are like 30, 10 and 30 percent chances. So we'll see what's happened, but it's good to get prepared. That's for sure. Yeah. Yeah. I mean, temperatures have been high.

I'm sure. The, you know, the situations are right for some storms. So just a matter of them making it here. Uh, it's usually inevitable that we get a couple, so. If you are, um, you know, a storm, a person, a storm restoration contractor, or maybe you're a retail guy who's thinking of dipping his toe in storms, or maybe you're in an area that's storm prone and, uh, you work storms when they actually hit your area, what do they call them?

Not storm chasers. Storm something else. I can't remember. They have a name for it. Oh, I know exactly what you're talking about. I can't remember the name. Ben from Roof Dagger told me, but I can't remember what the name of it is. When you work storms that are only in your area. Uh, I can't remember what he called it, but, but anyway, so, um, so yeah, I mean, regardless of your situation and the type of, uh, you know, the type of business that you're running.

Storms can obviously be either a huge part of your business or a nice little addition to, you know, especially this time of the year, we're kind of, you know, if you're a retail roofer, like we're kind of wrapping down retail season now, uh, you know, starting to get into the cooler weather. If you're up North, things are going to start to slow a little bit.

This could literally be a boost for you, uh, you know, to, If there's a storm coming through and you're able to work it. So big time. And just like it could be your season that you can make your money or just going to top off. If you're not prepared for it properly, it could be a huge mess. And it can really mess it up like everywhere from obviously lost revenue and lost opportunity.

But if you do not run that storm properly, there could be. Legal consequences, company consequences and stuff like that. So you want to be ahead of that. And that's kind of why we were looking at doing the, this two part series here is kind of prepping you for storm season, just so that you're up and ready and ready to rock and roll.

No pun intended. I have to say it now. So you can win the storm. So there you go. Josie would be proud of you. Yeah. So, I mean, let's, let's talk a little bit about it. You know, the biggest differences that we see. From your regular everyday retail roofer to what we see these storm guys doing. Like obviously you talked about legality.

That would be probably the first thing that comes to my, my mind is there's, especially like if you're in Florida right now, uh, you know, or a place like that, you know, there's legally, There are some very, very specific things that need to happen if you're working with, uh, an insurance type of roof situation.

Yeah. And you're seeing the laws change as, as we go along. So Florida is a great point. They last year launched a new initiative or new law rather called the good faith estimate law. And now as of August 1st, it's alive in, uh, Minnesota. And we can kind of see the right thing on the wall. It's insurance companies and insurance carriers and stuff.

They make the laws and they kind of pile it in one area and then it starts to expand. So I would highly I would say that we're going to see that goal nationwide sooner rather than later there. So It's important to take a look at something like that. Like that's a great starting point on what you need to do to make sure that you're kind of set up for the storm.

Cause that's the initial contact, right? Pete, like that's what we need to do to get that lead. And if you don't follow that, you could be at risk for penalties, whether it's not getting the job, having insurance, the rest of your insurance jobs with that carrier, not being looked at, or even fines as well.

Yeah, it's interesting. You know, I had a conversation with Corey Combs of South Shore Roofing. He's our roofer of the month for September coming up and uh, did a podcast with him last week and we were talking a bit about insurance roofing and he was saying, you know, the one thing about the insurance companies is every time the roofers find a way to, I don't want to say exploit, but take advantage a bit of the situation.

Yeah, exactly. Find a loophole that allows us to, you know, maybe make a little bit more on a job or something like that. They are going to essentially counter that. Right. And so, uh, the good faith estimate is something that they've had in Florida and now they're kind of pushing it other places. Um, you know, I know talking to some of the guys that it's been a big part of what they do in Florida for a little bit.

Um, you know, so like you said, I think the writing's on the wall there, that's going to become a nationwide. And, you know, and I think that's like right out of the box, you know, if you are going to tackle any kind of storm work, make sure, you know, What you got going on? Cause it is specific to your state. I know, I think Minnesota now and Texas have specific clauses that have to be in your contract.

They have to be bolded. They have to be highlighted all of these things, right? Make sure you're covered. Make sure you've got the legal end down before you, you know, venture any further into it. But, uh, yeah, let's, let's start right there, Nick. You know, we talked about. You know, the good faith estimate is the, is the new thing, right?

Um, in a lot of States coming up, uh, effective right now in Minnesota, you know, let's talk about how Roofer can help from the good faith estimate standpoint. You know, this, this is obviously something that I think, like you said, is going to gain traction and become probably the status quo everywhere. So, you know, what can we possibly do to, to help the contractor with those good faith estimates?

Yeah, like if we're looking at the law of it, it's basically it's saying, uh, a, uh, a company is required to give homeowners a good faith estimate that breaks down its cost and services and materials before they sign a repair agreement. And that's really not hard to do. Like, if you think about like traditionally, if you door knock at them to sign a contingency, and then you go up on the roof and you start doing it.

You know, taking the photos, doing the inspection and supplementing. Now that has kind of a blocker there. So you need to provide that. Now, realistically, are you going to sit in the driveway and write out a quote, a line item quote on your iPad, on a piece of paper, and then getting them up there and showing it to them?

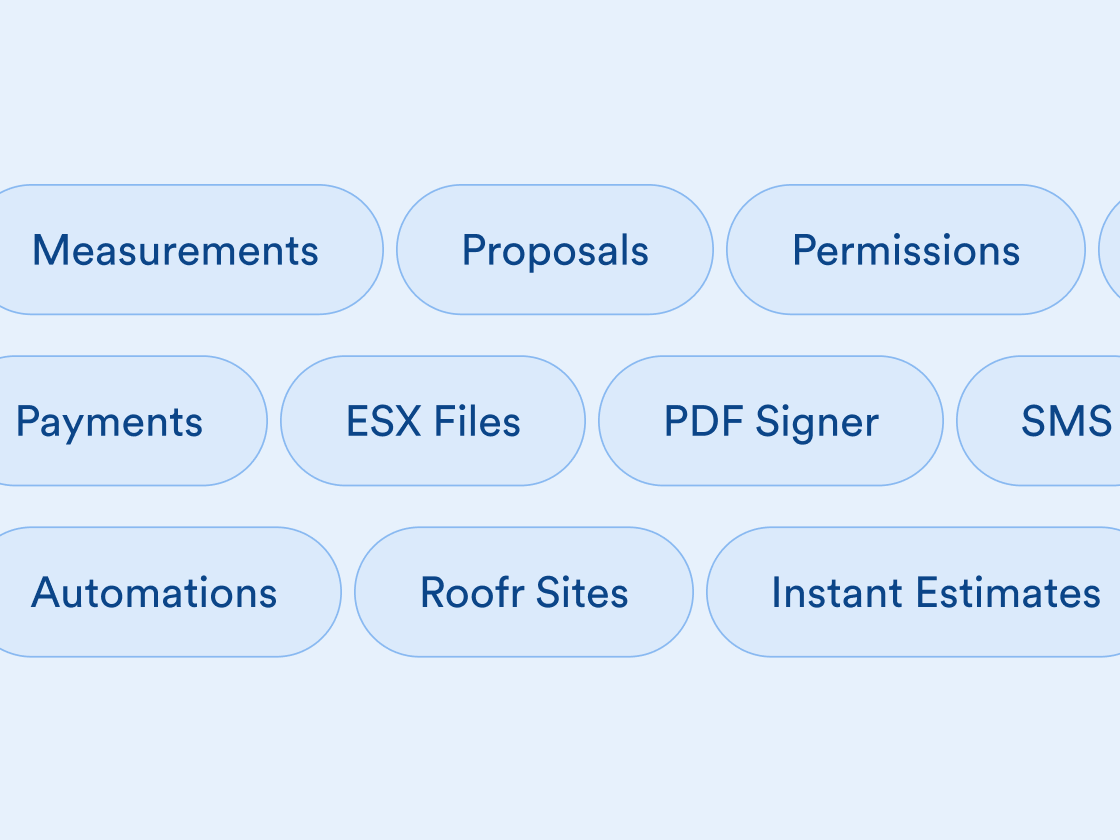

Probably not. It's going to take you some time. And a lot of people might just skirt around that law and just decide not to do that. But again, you don't want to get caught with this stuff. It's super simple to kind of find a solution for it. And. Truthfully, our instant estimator is that solution. Like you can have your instant estimator be customized to your options, giving them a lump sum payment, a lump sum option.

With financing involved, along with that square footage count, rough square footage count, and in the customization at the bottom, you can really create a line item quote with a clause, format it, and bing bang boom, it's there, and it's easy to get that in front of them. So now, when you're door knocking, when you're doing mailers, if it's on your website, if it's a flyer, whatever the case may be, They go on to that or you show them on their phone and provide it in front of them is a good faith estimate And it's emailed to them time stamp and everything So you are protected and then go ahead do the your inspection and get the contingency order some measurements We got some updates to our measurements as well that we go talk about later on either today or in the next part but making sure you have that good faith estimate lined in and that you have something that can Clearly, uh, break down the scope of everything and the materials and everything else like that is going to be super imperative for you to kind of take on that storm.

Yeah. And the beauty of it too, is it plays right into our whole speed to lead, which you and I talk about quite often is even more important depending on your market, right? Uh, it may be huge for retail as well in your market, you know, to get to that customer first, but it's very imperative when we have a storm, right?

Every. When a storm hits an area, you know, let's say it's hail, right? Like these guys that work hail, you know, hail could be down literally to a street or two, right? And now these guys, everyone knows they got hit by hail. They're going to get flooded with quotes. So what, what are you doing to set yourself apart?

Speed to lead? What is it? Seven, you're seven times more likely to win the contract if you're the first person in the door, right? And so it's like, you know, like getting there and being able to get that good faith estimate in their hands as quick as possible. Makes all the difference, right? It's, it could be the difference between you winning and losing that job specifically, uh, just because you're able to get there quickly and you're able to provide what they need, right?

It's not a situation where you're showing up and then you're having to leave, right? Like Nick said, go back to your truck, write up a quote, come back another time, maybe to present it or to give it to them. You know, you could have lost a job in that timeframe. Uh, you know, if the other guy's doing it more efficiently or a little quicker.

So, you know, having the ability to utilize. That instant estimator to instantly knock out that good faith estimate, leave that, put that in their hand. You know, now you can go about your business and doing your, uh, you know, your inspection and things, but now you've planted that seed, right? You've got something of substance.

Like you said, it emails it to them. They're ready to go. It's something that they can go back and look at, you know, if other people are coming to the door and like I always said, I'd rather be the first one in the door that everyone else is getting compared to than the last one in the door getting compared to everyone else.

Right. So, you know, if you can leave something that's polished and professional, Right out of the box that everyone else is going to get, uh, you know, compared to when they, when it comes to quotes, you know, that you've already won, you know? So, um, you know, I think it's, it's super smart. It, like you said, it solves a major issue that is going to, I think, become, you know, kind of the status quo here across the board with the good faith estimates.

So, uh, you know, the IE really is a game changer when it comes to storm season big time. And you mentioned earlier, like even if you're a retail guy, dipping your toes into storm. This works for both sides. The fact that it is a, it's an estimate, doesn't mean that it's just made for insurance, but at least you're compliant with both sides there.

You're able to take it on, understand everything, and break it down from there. So creating it for your retail business. Corey comes as a perfect example. Someone in a insurance market that only does retail. But you have those options available. So having yourself kind of set up with that, it's easy to rock and roll and you can take it to the next step.

And that speed to lead is everything. So not only are you going to get to them quicker, 30 seconds, it's pretty darn quick, but you're also going to be able to open up that door to have a little bit more options when it comes to, um, what's the next steps, right. And separating yourself from the competition.

Cause. Like everyone's being compared to you and you were able to give a quote in 30 seconds with six different options. Scope will work, where they can select and take a look at a carousel, get a soft pull and book an appointment, a soft financing pull and book an appointment. Is anybody else doing that in your market?

And if so, you better want to get, you want to compete with them as well. So that's going to be a big part. Yeah, absolutely. Well, let's talk about the proposal side, right? So we've gone, we've run our, uh, you know, we've run our appointment, we've done our inspection, and now it's time to present a proposal.

And so, you know, obviously Roofr has built an incredible proposal tool. It's probably one of my favorite pieces of the product, all of the functionality that it has, and all the things it can do. Let's talk a little bit about What you see are the biggest advantages that the proposal gives you when it comes to the insurance side of things.

I know, uh, you know, you mentioned right off the bat. One thing that comes to my mind is the multiple options, right? Like having the ability to kind of give them some selections and, and, and empower the customer, you know, as to what they're picking, you know, Uh, to use the words out of your book, to, to educate them, right, to use your transparency and educate them on, you know, uh, on what they're doing with a roof.

You know, the thing about these storm markets too, is if you're in an area that is consistently getting hit by storms, these are probably pretty smart buyers, right? Like these are probably people that are not their first rodeo. Like they've been through this before. You know, they've seen a storm or two, they may have already replaced their roof once or twice.

You know, they kind of know a little bit more than the average person, uh, is going to know. So, uh, you know, being super polished, being very educational and transparent about what you've got going on, uh, you know, very informative with the proposal, I think are huge pieces. What, what do you think, Nick, are some of the biggest advantages to our proposal to when it comes to the insurance side?

Well, it comes down to diversity. Like how are you running yourself? If you're an insurance contractor, what is your sales process like? You and I spoke to a guy named Steve, uh, last week, uh, from, uh, Houston and running Synergy, uh, roofing company there. And he was, it was really interesting to see that he's a full insurance roofer and he builds out his proposals like a retail bid, but he has his clauses up front and he's got his contract in the back and everything in between.

And he wins a lot of jobs and he's been growing rapidly in that time because, you He creates an informative kind of presentation and step by step. So when he's up against someone who's just strictly using Xactimate, it's apples and oranges, right? Xactimate looks like a different language, but it's important to use and that will be the second part of my answer here.

But at the end of the day, when you're talking to that homeowner, the homeowner is the policyholder. And you want to make sure that you're making them feel comfortable, that you're the right choice for them, that you can answer all those questions, and that you can leave that value behind. That's my biggest thing is to leave the value behind because you can talk to them and talk, express your value and show them how you're the right choice.

But ultimately, when you leave that door, they're going to be talking amongst each other, the homeowners, and they're not going to be able to say everything the same way that you did. They might've forgotten something or misunderstood something. And if you have a nice presentation proposal, you can leave that value behind for them to kind of refer back to.

So that's a one big thing right off the bat is being able to show that up front. And if you're doing it like a lump sum way, just like that guy, Steve is, it's a really awesome way to kind of change that flow. The other option is kind of working with Xactimate. If you're an Xactimate user, because you're in a Restoration Roofer, There's no problem with it.

I'm not like I always say Pete Pete's heard me say it before is We're not trying to reinvent the wheel here. We're just trying to take your wood spokes put steel on them So we're just updating your process And a good way of updating it is We know Xactimate is the king in insurance markets and you're going to need that for the adjuster because that's what they're familiar with.

Where I've seen a lot of roofers do this and Michael Miller, uh, used to do this a lot and that's kind of where I got this is use the Roofer proposal because how quick and easy it is to pull from a measurement and create this beautiful presentation style proposal as Your intro to get that contract signed to win over that trucks and get that a a or not It'll be but the contingency sign and ready to rock on that and what he did was it was a very presentation style proposal He had three options that the customer were interested in and for the description He would put the RFD code or the f9 and from Xactimate And then turned on all the options for quantity, um, line item total, and, uh, unit total.

So it would kind of mimic an Xactimate. At the same time, it would still build an Xactimate so that when you talk to the adjuster, He had something for that to help supplement and increase his actual sales. But that first thing was able to educate the homeowner, talk to them like a human being, let them understand what's going on, it's not looking like a different language like Xactimate.

If an adjuster got a hold of that, it would still be talking his language with the RFG code, the line items written out exactly the same way. And the items in there. So that's a really great way of doing that. And then the third and final one that I've seen work really well. Shout out to John Tucker, um, for fronting roofing out in, uh, close to you now, B.

He's like in between, uh, the, the, uh, Tennessee to Kentucky border. So, um, probably not far, but what he's done is he built up presentation style proposals that walks everybody through it. He actually sends videos of him going through it with each one of the customers in the email, which is a really nice touch.

But what he does is he puts the policy holder as the main signature and puts the adjuster as the cosigner. So that at that point, he can see the adjuster opening it. The adjuster cannot change the choices, they can just sign off and agree. So that now he has data on how many times the adjuster has looked at it or the carrier has looked at it.

what days, what times and is able to really kind of bring in his power for that and talk to the policy holder and get them to push their way around rather than him as a Roofer. I love that. Yeah. You don't, I don't know if that's something that everybody understands that Roofer does, you know, but Roofer tracks the, you know, the status of your proposal.

And one of the big things that it does is it shows you, You know, when people are viewing it, when they're, uh, opening it. So, you know, and this is a great use case of it, right? Like I, I think, you know, traditionally we think of it like, Oh, you send it to the homeowner. I want to see what the homeowner is looking at it, but this is a really great twist that John is doing where he's utilizing it kind of against the, not against, but, you know, to his advantage against the, um, The adjuster to be able to see what's, what's the adjuster doing with this, right?

So then I can be a little bit more proactive in pushing that guy to get this thing taken care of and get the ball moving on it, right? So we know that they can traditionally be a log jam there, uh, you know, getting adjusters to approve things. So he's figured out a way to manipulate. Our proposal tool to help him speed up that process and make it more streamlined for him.

So super smart use of the platform, which is really good because ultimately all three of those different scenarios, all are using it as building trust. Leaving value, creating that policyholder to roofer relationship so that they can go to bat for you and you could then submit the supplements after, create some upgrade options to increase your bid, whatever you kind of want to build out.

So I think the first step that you'd have to look at before we, because our team will help you build those proposals as well, is what kind of insurance roofer are you? Are you one that goes off the scope of work from insurance? Are you looking to supplement and only work off the Xactimate? Or are you building up the lump sum options?

Or is that a mix in between? Because if you have that there, we can start to build that proposal to fit your need and really allow you to kind of really capitalize on any storm that's there. But realistically, what you're here for, what you're in roofing for is to help that homeowner make some money while you're doing it.

And this will help you do that. Yeah. And you brought up something, uh, earlier you said, you know, you want to manipulate the proposal tool to work for you inside of your process. Right. And so let's shift a little bit and talk about that. Obviously my favorite part, right. Is the process is setting that up.

And I love what we've been able to do because I think, you know, traditionally when we were in these other CRMs. You know, you have your workflow, you're like, well, I'm a retail roofer. I have a workflow set up for retail roofing. I can't necessarily just shift gears and change my whole workflow to accommodate insurance.

You know, there's stages in there that things that we do that don't apply to my everyday retail work. I don't want to have to add them because maybe insurance is not a big part of your day, or maybe the opposite, you know, maybe you just don't want your insurance and your retail kind of intermixing, you know, and so many of the other platforms kind of.

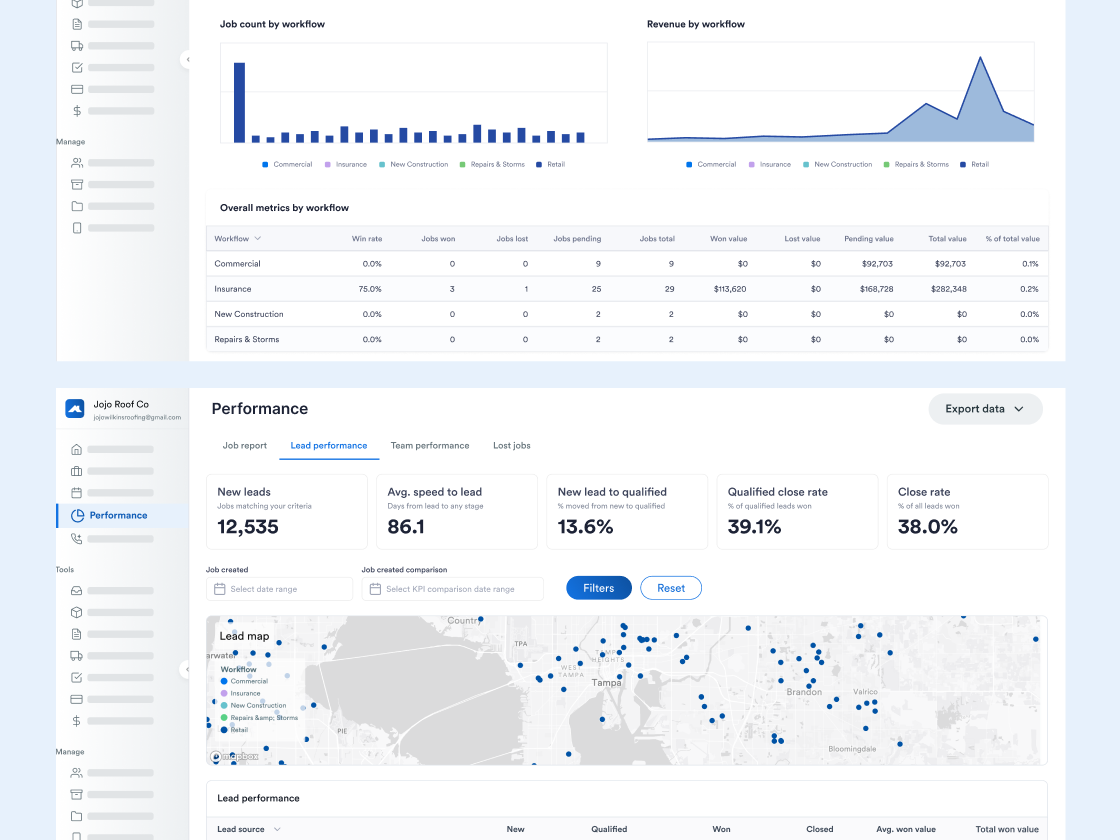

Kind of force you to do that just with the way they're set up, right? They, you don't really have a choice. You kind of have to, you know, put them into the same workflow and, you know, or have stages that you're constantly skipping over when you're doing retail work or, or something else. So, uh, obviously one of my favorite pieces is our job board and it really dials in your system and processes here and what we've done.

To help the insurance guy or the guy who is maybe doing both, right? Retail and insurance. We see a ton of that. Um, so we accommodate it, right? So we built out the ability to have multiple workflows, uh, and they can run simultaneously, right? So you can essentially assign a job to the specific workflow.

We've got the ability to have three. You know, you got your retail, you got your insurance, you got your repairs. Uh, those are the three big boys to start with. And so now when a job comes in, you know, if it's storm season and now all of a sudden I'm a normally a retail guy, but hey, we got hit by a storm, we're going to be working these insurance jobs.

Or maybe we go to a retail job and realize That it could be, you know, that we can file a claim for this. It's got damage from a recent storm and we can turn this into an insurance job. Here quickly. We have the ability to adjust that job and now send it into a completely separate workflow that has unique stages to that specific workflow.

So I love that. I love having them running parallel to each other. I love the ability. To toggle the jobs between them. So like I said, if you go out to a regular retail job and now all of a sudden it becomes insurance based, you know, based on some damage you find, you can quickly just reassign it, put it in that other workflow.

Yeah, it makes a big difference there. So like if you were having that situation where, Hey, I'm retail first or insurance first, and it goes to retail or I'm retail first, and I see that it's insurance. You can quickly move that over to change that work workflow to a new spot and add that in. And then all of a sudden, if I go back into my insurance workflow, I'll just turn them both on at the same time here, you're able to see that that's now in here and we have everything kind of opened up on it.

So you're able to see which ones are which, where they're coming from and everything else in there. And to Pete's point, different, uh, uh, workflows have different stages. There was different, it's not the same process over and over. So with this on the elite plan, you can create as many, you could create three pipelines, as many.

Stages as you want. Now we don't want to go too crazy because as Pete said, we never want to make it too granular where you can get lost in the sauce, but, and you can turn on and off different stages for each, each, uh, workflow. So as you can see, for insurance, it's a little bit more granular than a retail, definitely more granular than repairs as well.

But you can see instead of just kind of appointment scheduled proposal, send and propose a follow up in my, um, Uh, my retail stage here. I have an appointment, scheduled inspection, contingency sign, adjuster meeting, adjust the followup, additional approval, blah, blah, blah. As we go along supplementing first payment, all that stuff broken down piece by piece, and you can make that there and customize it, turn things on and off very easily and move things around and reassign things that need to be in there so that when you're viewing it, you can either view your job board as a single option here.

So, or multiple, as you can see, if I have multiple, I have little badges to show me which is which and which pipeline each one lives in. So I can walk through this and see, all right, I got all this information in here. Here's this insurance job which is here, and I can go in and make that flow, move it across that thing as I need, and open up that door.

We're able to even filter different things as well. Make sure that I have everything signed, lined up the way I want it. Make sure I'm seeing the stages that I need to see and really kind of either have things move over through automation or manually move them. You can build that up very, very easily here.

Yeah. I mean, I, I just love the fact that it separates them out. Right. And I think traditionally people think like, Oh, this is for big companies that have separate divisions. But it's not, right? Like it's actually just as beneficial, if not more beneficial for someone who's running a smaller business to stay super organized and be able to break these out and really see what's going on.

Uh, you know, across the different types of work that they're doing. Um, a question for you here, Uh, Nick, uh, Sean asked, is there a way to set up a time and material proposal for repair work? Ooh, good, great question. So with that aspect there, you can definitely add in time and material proposals. I have a couple here that I've built out.

Uh, one of which is kind of inspection and repair template where you can kind of build in like your suggestions and what to do and build that in there for quote, along with providing like super detailed photos and breakdown of everything as well. But the one I like to use the most is this one here. You could break it down piece by piece and really set up that time.

So you can have your clock on site really kind of put in like an hourly rate in there and create that proposal. So let's just create one off this here. Real quick. And I always like to give options on those proposals as well. So number one, we have some option here. I have a roof maintenance program as an option as well.

I have a full replacement option as well. And if I go in here and I want to add in something like an hourly repair, I don't have it in my catalog, but I can add things from my catalog and say that it is 100 an hour and that took me four hours to do. Yeah, we could add that in. We could show everything that's broken down piece by piece here and even see any upgrade options that in there as well.

We could build in our profitability that I need to be in here, so let's just say 430 percent seems aggressive, so let's go to 40%. Um, could be making good money on that, but you can see everything broken down piece by piece here and everything's broken down here. Let's go for option one here. Everything else is going to be mapped.

I don't have any flat on this job, so I'll just take that flat out. And the full shingle replacement is already pieced out perfectly here with all my additional upgrades. So what I can do now is, in seconds, provide something really, really, uh, precise and beautiful for that client to take a look at. Talk a little bit about you.

We build out about us pages for you. And a breakdown of the shingle repair option that I can do, or how long it's going to take me. Or a full replacement and really break that down piece by piece with all the options. And now they can kind of see like, okay, cool. I could pay 30, 000 plus some upgrades to do this.

Or I can do the shingle repair option and Pete's favorite creative roof maintenance program. So that quarterly, I come in there and take a look at it. You can even see that you can leave details and everything here. 750 a year costs, making sure I do spot repairs and everything else. Then a little touch up brochure on like, Hey, what, what is a repair?

Here's full replacement options. Here's some of the reasons you need repairs. We've got some big blow offs and everything else here, but in a matter of seconds, the customer can come in, pick the options that they want. Maybe it's the upgrade here. And now we're ready to rock with the signing and good to go.

So you can really, again, not to say that it's fully malleable, but you can manipulate this very, very easily and provide value. And if you want to be like that, uh, where you can show up the subtotals quantity and unit prices, you can add that in there to provide a little bit more transparency if need be and see how everything is broken down as well.

Yeah. And I mean, and this kind of plays into talking about a little bit about templates, right? Like, so templates are really allowing you to have, you know, these preset contracts. Depending on the type of work you're doing. So if you're like, again, if you're a retail guy, that's mixing in some insurance, you know, and maybe day to day you're do writing a bunch of retail quotes, you know, but now, you know, Hey, we're getting hit by a storm.

We're going to need an insurance contract. Verbiage is totally different. Like we got to have some other information in there. We've got to have some extra stuff. You can easily build out a template. Like you saw Nick scrolling through. We have a bunch in here. Uh, you can easily build out a template that is separate.

You know, separates out, uh, you know, your insurance information from your retail stuff, and you can run with that, uh, you know, out in the field. So it's, uh, you know, I really liked the fact of dropping the pictures in, like you said, the way Sean or, um, Steve was using it where he had the, um, You know, he had all of his information, kind of his inspection and everything in there, his contract down at the bottom, you know, so he got all his clauses and all this important information out of the way up top.

And then he had his, uh, you know, the nuts and bolts of the contract down, down there at the bottom. So, uh, really interesting. Way of setting things up, but you have that flexibility, you know, you can really dial this in to be exactly what you need to fit the situation. Yeah. And like, this is one of the insurance options I was showing you where you can put in the RFP codes, a la Mike Miller that showed us, so you can see how you can break this down a nice presentation of everything, and then you can have it broken down with section headings.

You have the exact naming, uh, that was in there with the RFP codes added in. Unit price, quantity, and subtotal listed right across the board here, plus upgrades. So you can see how that all breaks down. You can create good, better, best, provide that transparency and education for that homeowner. And then ultimately show them what's going on.

Another benefit of this too, is if you're, if you're arguing at the adjuster, hopefully you're not, but if you are, you, they say like a lot of times I hear a hip and ridges included in waste and starters. It's like, well, no, sir. If you'd kind of look at the. I'm a, I'm a certified installer for OC, like you can see right here that these are five different spots of the roof that I need to install to make sure that I have that warranty.

So you can have that information provided in there, breaking down piece by piece along the way. And then you could also like throw in your contracts in here. So you could have your initials, full signatures, photos like Pete said. You can put in the building code if you need to, right? Have the building code in there so you can refer back to that stuff.

You can make this as long as in short as you need it, but you're going to be able to present this in a much better way to show them how things move and it's interactive. You're separating yourself from the competition and you're going to get this all lined in very, very quickly. So you can see how it will flow right across this entire thing to make sure you're protected, they're protected and the insurance stuff is done.

And as Pete mentioned, you see on, on, on my templates, I had some retail ones. I had some insurance ones. I had some. Repair ones all broken down piece by piece to open that door up and allow me to be a lot more versatile with how I'm running things. Yeah. I love this. I love the way that this is set up and, and the way it flows.

And let's talk about while we're in here right. Financing a little bit. You know, financing is huge on the insurance side a lot of times. Uh, the ability to tie financing in, right? Yeah. And we have a great partnership with, uh, well there's two ways of doing it. One of them, we written the proposal here is we have a great partnership with Good Leap.

And with Goodleaf, you could put this pricing directly in here. So let's, uh, excuse my crazy screen here, but I have it here where you can show it directly in that quote and you can finance that deductible maybe, or you can finance that entire job if you're doing retail and stuff like that, battling insurance in the market, just like Corey Combs did.

You can have that built in where they can apply directly in the quote and we'll show you how much the options are as they're selecting it, that will change up as well. We will have more financing partners in the future, but that's just a one quick way to show it. But then the other way of breaking it down is in the instant estimator.

You can put it inside your instant estimate. Here's a good faith example here where I can actually have my financing link directly in here. So you could break it down piece by piece, opening that up and kind of create some customization. Little sneak peek here. We just added social media links directly to your proposal as well.

So, uh, your instant estimator as well. So. Instead of doing financing and starting that conversation after the big numbers presented in front of them, why not kind of build it in here where you can actually have it from the start, where you can get soft pulls and everything broken in there right away to show some options.

So if they go through this flow, speeding it through just to provide this, this is what your good faith estimate can look like where you're showing options here and financing options, and they can click here directly and apply for financing directly in there. So that allows you to be a lot more agile with this stuff.

And again, here's your material line item quote there with a nice little bold section, like Pete said, breaking down some lump sum options here for your good faith estimate, have your company can projects in there and your fun little socials in here too. So that will open that up, but you're really able to kind of make sure that you're set up for that storm.

If you have that financing lined in. Yeah. And one of the things that I like is, you know, I think the key, obviously when you're dealing with these insurance companies is. The more information, the better, right? Like you want to start to build this portfolio of information. It starts here. You know, you have a very detailed, as you can see a very detailed good faith estimate here that you're putting in front of the customer.

That's kind of the start of a really nice package of, uh, information that you're going to be able to provide them. Uh, and this flows right into like our proposal tool and all the things that our proposal tool allows you to do. You know, Nick showed one earlier where he was dropping pictures in there and doing an inspection form.

You know, you've got, um, you know, he, he showed the brochure showing exactly the roofing pieces, you know, so you could get very detailed in this presentation style, uh, proposal to where it becomes almost like a portfolio of information. Now, you know, you can tie in the measurement report, you know, if you're pulling the measurement report through us, you could tie that in and drop it as a page or multiple pages on the, uh, on the actual proposal.

So, you know, you're, you're not only, you're building a really nice presentation for the. Customer to be able to sell them. With, but you're building a really nice portfolio of information together about the job for the homeowner or for the, uh, the insurance company themselves. Right. So, uh, you know, I really like that, how it kind of pulls it all together because I think, you know, normally we're, we're kind of getting, you know, we're getting measurements here and we're getting some information from over here about the house and we've probably got inspection photos and another software, maybe it's company cam, right.

Right. We have a company cam integration, so now you can bring those pictures in and utilize them here. So you know, it's kind of bringing all of those systems together to produce this one really nice document. Yeah, it makes it super easy to build that and you can see the different options here.

Uploading these are very easy. Um, I'll just go into some Roof photos here and just show you kind of how that would open. So I can quickly just add these photos in there if you have that inspection process. I know that I quickly mentioned that before. We have all these options here. I'm going to quickly edit this.

I'm going to drop in the numbers. If you have CompanyCam, you can actually upload the annotated images already in there. So you don't have to do this part in Roofer. But this is also, if you don't have CompanyCam, this is how you can do this in Roofer as well. So I can really open up that there. Tilt it across.

Showing some issues. One last issue I will show is here. Hit save on this, and then I can add a description saying like, Leaking because the last roofer sucked. And there you go. So you add that in, you have this breakdown. And when you preview and send this, I could even put in my, you know, about us, a breakdown of all these different photos, piece by piece, how this goes along.

I can put in my suggestions with the cost on there, so if you're doing that up front, again, this adheres for good faith. So you have everything broken down piece by piece, different options, roof maintenance obviously, and then the customer can choose the differences between there. So you can really present well throughout that process, and as Pete said, add that measurement directly in there.

And don't add all the pages. You can see some of the pages of this report are hidden. You could hide with our system. You never want to send all of them too much. There's, there's such a thing as too much information. So you could add that directly in and hide pages as you can see here. Yeah, really like this.

And it helps, you know, just to keep your team organized as well. One of the things I wanted to kind of jump to really quick, Nick, is we kind of touched on the workflow. We talked about touching on multiple workflows and something came to mind and then we kind of went to proposals here, but checklists.

Yes. Right. You know, there's so many important things that we're dealing with when, and it kind of leads back to, it ties back to this whole part of, you know, we're building this portfolio of information, right? So we want to make sure that we're getting specific information from the customer, we're getting, uh, you know, their policy information, we're getting photos of the damage, right?

Like all these things that we want to make sure. Our team is getting out in the field. How do we do that without somebody slipping through the cracks checklist, right? We have the ability to create these automated lists of tasks that can be triggered off of a specific stage, off of a specific event, right?

So as the job is moving through our workflow, our process, it's triggering these checklists so that the team is not missing anything, right? We can assign these items. We can create due dates around them. They're time sensitive. Uh, you know, if the insurance companies that have certain information by a certain time, we can go ahead and we can add that in.

Um, so these become incredibly valuable, uh, to keeping the team on track and to making sure we get. Consistently get the information that we need. Um, you know, and, and one of the things like one of the best use cases, I saw this as a customer at a South Carolina who did a lot of storms, he did a lot of, uh, insurance, majority insurance work.

And there was a lot of things that he liked his team to cover. With the homeowner and it was simple stuff. It was, you know, it was things like, um, you know, just making sure that they understood that, you know, they weren't responsible for protecting the rose bushes from stuff calling off the roof, you know, like down to something that simple as, as well as, you know, some of the more high level stuff around, you know, working with the insurance company and stuff.

He built a checklist and it was twofold, right? It was for the homeowners. Knowledge, right. And, and to make sure that the homeowner had a good understanding, but it was also to make sure he actually built a checklist and then had his team make sure that it got initialed, right. It was actually built into and ended up built into his contract so that he could get initials from the homeowner.

And he said it was just as much to make sure that his team was reviewing all those items. Right. So, so just great ways to kind of keep everybody honest, right. Hold everybody a little bit accountable, but at the same time, be able to make sure. That we're doing all the stuff that we need, uh, you know, to produce the right documentation and, and have the right information for the, uh, you know, for the adjuster, as well as the claim, the homeowner, everybody involved.

Yeah, and like going back to your previous point about the process, you don't want to make it too granulated where it's difficult for a sales rep to follow, but this way, having it built directly in with automated tasks for step by step on each stage allows you to get granular without having to, you know, overwhelm someone.

So adding things in with due dates and assignees and stuff like that, as you saw, I just moved it over to a new stage and as we'll see. This will open up where we have more options here. So we have another bunch of, uh, uh, things pop have popped in for us to go through and you can see how that goes across.

You can even see how things, when things were completed directly in here too, so you could hold people accountable and make sure that you're covered. But so great way to kind of set you guys up for success. Fun fact, we have a browse automation page for like recommended by Roofr, uh, automations. And we can start building that in directly here.

Oh, maybe not that one. It was this one. Uh, click on the one right beside it. Uh, but you can see, you can immediately send this stuff over and create these tasks here, um, and add more in and create those automations so that each stage you have tasks built in. I have a ton built in on this because it's a demo account, but you can, we went through a whole automation.

Uh, uh, masterclass right before, but as you can see here, this is another way of doing it. And last but not least, Pete, but you mentioned that one thing where, um, they have it in their contract as well. I'm wondering if I have it in this template, but I know that exact thing you were talking about because, oh yeah, your installation includes, you could have everything broken down with initials beside each part there.

And then even in terms of conditions, same thing. Step by step to make sure you're protected and the homeowner is protected. Think about it both ways. It's not just a one way street there. You're providing that value and that referral that you're building from this trust is going to allow you to acquire more customers down the line at a very low cost.

Minimal cost because that's going to open that up there too. So you can see piece by piece across this board. So then when the customer is looking to sign, I got Tom Hawkins here, he's agreeing on this inspection and they can go through. And as we're going to cross it, I can make sure that they understand that it's 15 per bundle, extra, if there's an extra layer, 90 per sheet here, and he's signing off on this, right?

10 day cancellation policy, 25 percent here, this, and this, and he just. The green to everything right here, which is nice. And then boom, up and running and you're ready to rock and roll. And that's just from like that initial inspection contract here. Everything's kind of in, in, in writing now. So a bunch of different ways, but I think.

The moral of the story, and we keep on coming back to it, is process, process, process. Isn't that right, Process Beat? That's correct, yeah. We do, we have a question here by Zach. He said, out of curiosity, where the name is. So I believe he's talking right there under the job details section. Um, he said there's an email with the email icon, the phone number icon.

He said, what does the gray, the green symbol mean versus a gray symbol? We're talking about right here, I'm assuming. Uh, I don't want to be talking about there or over on the left. Maybe you see how that's lit up proposal and report green. I'm thinking that's where he means. Exactly. Just comment. If it is, well, you know what?

We'll just, yeah, there you go. He said, yes. Okay, cool. So here, this is going to show you the stages that things are in number one. So, uh, we'll come back to the numbers and stuff after, but, uh, On the side. If I go into this right off the bat, there is no, he said under the name, I think you were right the first time.

Darn it. I knew he said yes, but he said no, but he said under the knee. All right, let me flip back over to, I want it. So I got to move over to one. I want to use that exact one. Okay, cool. So here, fun fact, there's a couple options here. So number one, the email means it's a real email, which is a shock to me.

Um, because I definitely emailed that email when I thought I created a fake one. So it's verifying that it's a real email and we can email it out. So some man got a quote. For a invisible address, uh, so who knows, but uh, yeah, so number one, if you're on your mobile, this will allow you to email directly from your device.

So quick jump there, as well as calling directly from your device. So if I do it on my phone here, I can open up my VIOP that I have for our company and, and, uh, dial that number. As you can see, But that's a good way of doing that. But the other thing is, is being able to copy that stuff as well. The screen check mark is here, but not here.

So if you actually go into this, You can actually see on here, let me just click here, I could edit this customer and I could record consent for texting as well. So if we, we, Roofr does have texting, so you can sign up actually right now for free, uh, while we're in our closed beta of it, uh, so you can sign up at any time, just talk to your rep.

If I go the customer agreed here and they did verbal and written verbal implicit or written one of it has to be at least one of those, I could click on those and you can see that I got a green checkmark. Now. Now, I think it was Zach. I could text this person and say, sup, do you like the Roofr. Probably don't talk to them like this, but that way you can send it.

It's not a real number. That's why. Um, but we can play around with all that stuff there. So you can see that and how it breaks down piece by piece and be able to go around with that. Let me actually just put in my cell phone so you can see how this works. I am getting no written, but I'll give you Verbal.

Access to it. Um, is Pete. Cool. Send this out. I will quickly check my phone as I get a response. There we go. It's on here. And I say, yeah, he's. And then if I refresh the page, we'll see that pop in. And now I have the texting right there. Let it load. So real time texting in the right hand corner there. And that check mark.

Uh, Zach is just gonna show you if they have, if you have recorded, that they have consented to text messaging. Very good. Um, looking to see if you have any other questions that we potentially missed here. Kyle asked when the calendar will be added. Stay tuned. That is, uh, around the corner. Yeah, yeah, around the corner here.

Upcoming meeting. Yeah. Yeah. We have a, uh, a masterclass student, I think about that exact topic. Exactly. Couldn't be more excited for that. How do I stop sharing? Stop sharing. Thank you guys. Screen inception there. Um, yeah, super excited for that calendar to come out. Um, What is it? The 24th? We're doing the master golf.

I believe so. Yes, I believe 24th. That's going to be exciting. So any other, any other big takeaways that we cover kind of jumped around a little bit today and covered a bunch of stuff, Nick, are there anything, any major things that you can think of that maybe we, uh, glanced over, uh, or just forgot completely that are really, really beneficial things that, um, you know, someone might want to take a look at if you're thinking of diving into storms this, uh, you know, this season.

I have two, three, three word advices. So number one, know your process, know your process, find out your process and put it in there and build it into your CRM. Hopefully you're using Roofr if you're not, build that process in there and make sure your team is up to date on that so that you do not have anything missed.

And then number two, know the laws. You've got to know the laws in your state, make sure that you're protected against all that stuff. Insurance, like we said, we find a loophole and then they close it. You got to understand guys, we're fighting against a trillion dollar industry. It's not a billion dollar industry, the trillion dollar industry.

So you want to make sure that you know that they're going to move the laws and you don't want to get blacklisted from it. It's a really good way to run your business and grow from it. And if you skirt the laws and get caught, it's not great. So just. Know the laws, fight for the laws, and then call out the bad players when you're, when you're talking to someone, right?

You talk to the homeowner, be like, hey, I'm following the laws here to make sure that we're protected. You got to pay your deductible, but I can finance it. This is a good to pay thanks that that person didn't give that to you. They could drop the insurance claim for you. So that's how you really protect yourself.

Yeah, I agree. I think big ones for me, obviously process, making sure that you understand the differences in your process. If you are, let's say a retail guy, obviously, like you said, it's going to be a little bit more granular. There's going to be a little bit more steps, you know, kind of dial that in, make sure that you're covering all your bases there.

And I love the checklist to make sure that we're not missing anything, right? I think that, you know, utilize the task, the automated tasks, utilize it as a checklist for your team to stay on task and to make sure that we're getting all the information that we need. The key to success on the insurance side is being detailed, having all that information, uh, you know, when they're asked for it and making sure that you're covered there.

Um, So I love using the tasks and using them as a checklist to keep everybody organized and on task and getting everything that we need. So, uh, those would be the big ones for me. And, uh, I believe we have a second part of this coming up next week, right? Yeah, exactly. We can dive into a little bit more of like adding temporary, uh, workers into your account so that if you're hiring people or canvassers or anything, be able to give them some restricted access, but still make sure that you're getting the data.

And, uh, we can dive into a little bit more. So, uh, if you have any questions, make sure you're here next week, for sure. Yeah. And the beauty of that is they cost nothing to add them in Roofr. Nothing. So I think your team with like, everyone has their own instant estimators. You can track how many leads that they're pulling in and not paying a dime extra for it.

Yeah, it's a beauty, especially if you're adding temporary help. Like Nick said, maybe you're adding just canvassers to, to work a storm that just hit or something, or, you know, you're adding some, you know, you're going to need some temporary help, you know, for the next couple of months to get through storm season, you know, and you want them on the platform and utilizing the products.

It's a great way to, to get them in there. Like Nick said, we can show you how to add some restricted access there. So, uh, you know, they're not living it up inside of your, uh, your CRM stuff. Moving things around. Yeah. Yeah. It's like a minority report. Yeah. Yeah. So, uh, so make sure you guys join us next time.

Uh, for jumping on with us today and, uh, there aren't any more questions, I guess, uh, we will see you guys next week on the Roofer masterclass for part two of, uh, Awesome. Be sure to be there, Jasmine. Talk to you. Yes. All right. Thank you guys.

Latest Masterclass

How to Get Commercial Roofing Jobs (with Bryan Mitchell)

Commercial roofing expert with 40+ years of experience, Bryan Mitchell, returns to share how to find, win, and succeed at commercial roofing work.

Unlock the Matrix with Performance Dashboards

Your whole roofing business lives in Roofr. Now, your reporting does too — and if you’re not sure how to best leverage it, let us show you how.

Customizing Your CRM to Match How You Do Business (Roofr Plans Explained)

Hosts Pete and Nic help four VERY REAL guest roofers find the right plan for their needs. Tune in if you could use a chuckle and want to learn more about Roofr.