The Rise of Retail Roofing with Chuck Allen

Fewer local adjusters, a stricter approval process, and more complicated regulations have pushed many roofers away from insurance work.

In this Masterclass, Pete and Nic sit down with seasoned roofer Chuck Allen to talk about what that shift looks like, why retail roofing has become the dominant model for many contractors, and how to make the transition or find a sustainable mix. The guys cover:

- Pros and cons of retail vs. insurance roofing

- Positioning your business for sustainability

- Avoiding cashflow risks and common pitfalls

- Handling depreciation as a retail roofer

- The importance of knowing your numbers

Tune in for an honest, insightful exploration of roofing in 2026 and how to adapt your own business to the realities of today.

Pete: All right. What's up everybody? Welcome back to the Roofr Masterclass. I am your host, Pete McKendrick, with my co-host, Nic, and we are joined today by honorary Roofr, Chuck Allen.

Chuck: Honorary. I love it. Well, that's- It's the first time honorary has actually been mentioned in the same sentence as my name.

So thank you guys. You've made my day already.

Pete: I figure you've been with us long enough, right? So welcome, Chuck. Excited to have you, man, and, this'll be a good one.

I think this is a topic that for the last couple years has been back and forth, right? You hear both sides of it obviously, and, so it'll be interesting to kinda get your take.

Nic: You know that me and Pete love talking the industry and, retail versus insurance, the age old battle. You got the host with the most, Pete McKendrick, and me Nic, just regular Nic. You can reach us anytime if you have any questions, anything that comes up. We had actually a couple people reach out the other week, which was cool, coming from the masterclass, uh. So pete@roofr.com and nic@roofr.com. And as a reminder, these are always recorded.

We host them at roofr.com/masterclass. What's nice about the YouTube ones, I didn't realize, but now they're segmented by topic too, so you can, like, speed across, find the spot that you're looking for, so.

Without further ado, the man, the myth, the legend, Chuck Allen.

Pete: Chuck, why don't we give you a second here to introduce yourself and, what you have going on, just in case there's anybody listening that doesn't know.

Chuck: Yeah, absolutely. So I'm Chuck Allen. San Antonio, Texas.

I own Rio Blanco Roofing and Restoration. I've been down here since 2019, but I've been in the industry 28 years. I also host the Keeping it Rio podcast, which is sponsored by Roofr for the last four years. I'm excited to chat about retail roofing today, 'cause it's definitely something near and dear to me, and I think that we've got a lot of cool information and perspectives that we can bring, and, hopefully we get a lot of participation from the crowd.

Pete: Yeah, Joel, I think you've got a couple polls you wanna run really quick. So go ahead and get those going while we start this chat up. We're getting more and more people that are doing a mix-

Chuck: Yeah

Pete: Is this

Chuck: a real time vote that's going on here?

Pete: Real time vote, yeah. Yeah Oh, nice. I like this Literally the numbers are changing as people are voting.

Chuck: Like this.

Nic: Me- me and Pete we always talk about it, like, the importance of diversification.

Like, if you're working your stocks or doing anything else, you gotta diversify. You can't put it all in one bucket. And there's, like, when you're talking about roofing, you have to diversify, and you need to split things up. My dad always used to have a saying that, retail's gonna keep the lights on, insurance will put you on vacation, and you can use that same framework for, residential and commercial, so that works out there.

But things change. We go through ebbs and flows. They're changing the goalpost with insurance. So it's always good to have that breakdown and have yourself qualified to do both, because different things come up, and you wanna be able to, you know, attack when the iron's hot.

Pete: Seven or eight years ago when I came into the industry, I remember this big divide, right? Like, you were either a retail guy or you were an insurance guy, and the insurance guys were like the cowboys of the industry, right?

It was like you did one or you did the other. You never really kinda dabbled in both. And so, obviously we've seen that change significantly. The majority of people doing one or the other here, almost equally retail to insurance as their main focus.

I always find it interesting how the industry continues to evolve. Like you said, Nic, there's so many things that are happening on the insurance side that are constantly changing and affecting how insurance is handled and how insurance is done in the industry.

So, obviously that's gonna change a lot of things.

Nic: And it depends on what state you're in too, right?

With good faith- Sure ... estimate laws coming in. I remember when we first started Roofr, I was living down in Florida running, leads after Irma, and just door knocking and signing AOBs like it was nothing. I remember looking at the guy that I was working with being like, "Dude, this is okay?" And he's just like, "Yeah.

You just sign it and it just they pay you." And I'm like, "It just seems weird that I'm just signing a piece of paper and everything's good." And he's just like, "Yeah. You just, have the customers, you just let them know on everything." And now we know that AOBs have changed. I, I don't think anywhere in the country that they're existing anymore, right?

So it's all contingency contracts and everything else. You see those goalposts moving as we go along.

Pete: Yeah, and, you know, we're already seeing comments about hurricane season and things like that. The weather plays such a huge part in this answer right here, right?

Yeah. Like, obviously very tough to rely on something that we don't control, right? You know, on the retail side at least we have some control. I'm sure Chuck's gonna dive a little bit into that. The insurance side is just so wide open, right? Like, we don't really control a lot of the factors that are involved in it, which makes it very difficult to predict and to forecast from a business standpoint.

What are your thoughts, Chuck, on some of those answers you saw there?

Chuck: Well, I mean, you guys are spot on. I've been doing this for a long time, and I remember, you know, 10, 12, 15 years ago when you'd just, ... You'd roll up to a house and it'd be, like, the same adjuster because you'd have, like, four or five local adjusters at that point.

You could build a relationship with them and they knew, "Okay, this guy's pretty honest." And, dare I say it was much easier back then because you could literally just roll up and be like, "Hey, Tom. What's up, buddy?" And Tom would be like, "Oh, okay. You know, you're good. Show me a little bit and we're gonna go ahead and take care of the homeowner."

It's definitely changed to the point now where when you used to go out to an adjuster meeting, you would actually go and you'd meet an adjuster, and you'd talk to the people, and you would know them. And now you get guys that go out there, and I'm not knocking anybody, but they're not licensed adjusters.

At the end of the day, they're sending people out to take photos and then send that to a, a neutral party that's sitting at a desk somewhere three or four states away, and that's going to be the determination as to whether or not that claim is gonna get paid out. And, when the question asks is it getting harder?

Yeah, it's definitely getting harder because that's, that wasn't the case 10 years ago. So I've seen the evolution, or whatever you wanna call it, and now it's to the point where I think over the next year, year and a half- It's done. Really as far as what we were accustomed to doing and seeing for all those years.

I think now is the time to develop that retail model because payouts are getting smaller, deductibles are getting way bigger.

Nic: Yeah.

Chuck: And, I've met three people this week already, it's Tuesday, that have gotten letters saying, "Your roof is old. You didn't even file a claim, but your roof is old, so you need to replace it out of pocket."

So okay, if that's the way that it's gonna be, then I think that it's time for everybody to, you know, kind of figure out exactly what we need to do and that was pretty badass. I'm gonna ask for that for my own podcast. Thank you. Yeah.

It's so hard right now as a contractor because, the payouts are getting smaller, they're getting more drawn out. Everything is harder as a contractor dealing with the insurance. Sometimes people like myself just look at that and say, "Man, I've been doing that for a long time and I'm, I'm not really enjoying it anymore."

So- Yeah ... we switched our model completely. We're doing straight retail in a Texas market, which is, you know, it's either crazy or genius. We'll figure that out later on down the road. But it's different because we're trying to, you know, stay ahead of that curve. I think if you're stuck on that model and you're still telling homeowners, "We'll do it for whatever the insurance pays.

All you'll have to pay is your deductible", and that's, you know, the good people. Some of them are, you know, still doing that nonsense about, free roof, this and that. But you get a 10 or $20,000 deductible, that changes everything. And now it's, it's survival of the fittest. So game on.

Nic: It's interesting too, like coming from Canada and growing up in Canada and running a roofing company up here, the way that insurance works up here is similar to what it's becoming in the United States.

So when I started working in running leads for roofing in the United States, I was like, "Man, this is wild. This is like the Wild, Wild West and everything's different." But in Canada what they do is essentially there is an insurance company. You have damage, the homeowner contacts the insurance company.

They contact a restoration company which is their preferred vendor. That preferred vendor puts out an RFP to contractors that they work with, roofers specifically, and get three bids presented to the homeowner. They pick one and then they go with it. And the margins are very similar to what you're alluding to, Chuck.

It's just a little bit above what retail is. You got a little bit of, of a bonus there. But what ends up happening up here is roofers don't wanna work for those restoration companies because payout is, net 90, net 120 or something like that and you're not- Yeah ... getting paid right away when if I'm doing retail and it's running the same price, my payout is job closed.

And throughout the years and as a Canadian watching what's happening in the in, in the States with the insurance, I just watch those goalposts just get narrower and narrower and narrower and now you're seeing some insurance companies having the preferred vendor program and yeah, it's different.

And I don't know if it's the worst thing in the world. I, like it's not great if you're fully into insurance, but if you can ingratiate yourself to those insurance companies and work with them, that's a lot of work that you can be getting. But it really comes down to that diversification like you're, y- like you did, Chuck, is just moving over to retail and seeing like that becoming the new norm is more contractors are building that aspect into their business.

Chuck: Yeah, I do think that that's gonna be a huge play in the future, is that there's gonna be some big players that are gonna take a huge chunk of that- ... insurance restoration market, and, you know, the mom and pops, the small time companies are gonna get that opportunity. But I think it's gonna be extremely painful really just because cash flow.

It's gonna kill a lot of those smaller companies that may be excited about that volume. You know, we're gonna give you three roofs a week guaranteed. That's cool until you, you need to pay the light bill, and two months down the road you still haven't gotten paid for the three you did the first week and you're now six, seven weeks in.

That can become very problematic as well. So it concerns me. I think that's gonna be a big thing, and I think there's gonna be a lot of opportunity for that work to be handed out that way. You know, I'd be happy to take some jobs here and there, but I don't think that's a good move to rely solely on if you wanna continue to grow.

If you're where you wanna be and you, you like the money and you're good, then yeah, absolutely. It's guaranteed work for the most part. So there's pluses and minuses, you know? Security versus ability to scale and grow and do more than just insurance work, which is kinda what I'm hoping to get into.

And, I think there's gonna be more than enough for everybody, but there'll definitely be some huge players in that insurance restoration/MRP type deal moving forward for sure. That's what all these private equity plays are about, I think.

Pete: Yeah, it's interesting, right? It takes a very unique roofing company to be able to float like that, right?

To be able to do a job and, be months down the road before I see any payout. That's not your everyday roofing company that's able to handle that. It's getting harder and harder to get paid out, and then you wait all that time, and now your margin is smaller than it could have potentially been.

And so, is it getting to the point where it doesn't necessarily make sense? Maybe it's great to supplement your process, right? And supplement what you're doing with it. Like you said, pick up some jobs here and there. But, you know, definitely changing from that all in on insurance model that we've traditionally seen.

Chuck: I think it's gonna be tough moving forward, I really do. And I, if that's your, your deal and you've been doing it for the last 20 years, it's been hugely successful, you know, there is an opportunity to make that pivot now. Unfortunately, I think a lot of people are gonna be stuck in their ways and they're gonna say, "No, this is the way it's been.

This is the way- Yeah ... it's always been and it's gonna stay that way." And it's gonna come back and bite pretty fast. It's good and bad. I mean, we're here in Texas, and we always have here in Texas the, uh, the house bill, the deductible bill that everybody loves to talk about that we've had here for, I don't know, six, seven years now.

And the thing about the deductible bill that nobody really ever mentioned was if you flip to page two, it clearly says in the deductible bill that the insurance carrier can waive a deductible at their discretion for any reason. So I have to collect it in full, it's that law, but they can go around and say, "Well, hey, if you use our preferred contractor who gives us good margins, good numbers, you can get it for free."

And at that point, what are you gonna do? You can't really be a legitimate contractor in that space at that time because nobody's gonna give you a $10,000 deductible when they say that, Home Depot or whoever the contractor of choice is, is willing to do it for no out-of-pocket expense,

Nic: it's hard to fight gratis.

Chuck: Yeah, right? I mean, I'd do it my damn self, and that's, that's being completely honest. Yeah. If it came down to that and I had to pay my deductible of, of five grand or seven grand or I could get someone to do the roof for me and I didn't even do my own house I'd maybe even think about that, honestly.

Pete: When you look at these companies traditionally that are, restoration contractors, they're potentially operating in multiple states, the amount of overhead that those businesses have, right?

The, multiple offices, tremendous amount of door knockers, which traditionally has a tremendous amount of turnover, right? Yeah. There's just a lot of things that don't get accounted for, right? Supplementing, do you handle it in-house? Do you third party it? Either way it's costing you extra money that you don't have on the retail side.

Talk a little bit, Chuck, about the differences that you've seen in that portion of the business.

Chuck: It really has been remarkable, and I always love and also kinda hate when you get a big storm that's fresh. I'm in San Antonio.

We haven't had any real major hail in over a year. So a lot of guys have been you know, training, doing their sales practice. Doing all this stuff, working for other companies. This storm hits and everybody all of a sudden is like, "Here we go. I'm gonna start my own company. I'm gonna go out here and do it."

And that's extremely dangerous because a lot of people don't really know about all the stuff on the other side that you have to take into account, and how fast you can get upside down. Let's say you just opened a roofing company, you get a, a credit line of 20 grand. That's three material orders maybe.

Maybe it's one if you do a really nice job and you get a big house, so you spend all your money on the front end. Now you have to wait for the insurance company to send the remainder of the money after the fact. In the meantime, your material bill is due. Your crew is certainly not waiting 60 to 90 days to get paid.

If you don't pay them by this afternoon, they're like, "We're coming to find you, sir." So you gotta take care of those. You've got your responsibilities, and you're upside down, you know, to the point where now you can't even go to the next job. That's as a startup. Now imagine you're a large company and you're doing, 40, 50 roofs a week, and you're doing that every single week consistently.

I mean, millions of dollars are just hanging out there, just waiting. And I think a lot of the cases where we see guys that, you know, have those bad stories about getting ripped off or having companies that screwed them over, I think most of that stuff starts out pretty innocently, and I think it's really more just a case of over ambition and just getting in too deep as a company.

I don't think anybody ever goes into it... Well, I mean, some people do, but I don't think a lot of people go into it thinking, "Man, I'm gonna screw a bunch of salespeople over. I'm not gonna be able to produce the jobs. Homeowners are gonna try to sue me. I'm gonna get a terrible reputation." It just is what happens when you get too involved, and it's very easy to get that involved.

That's the biggest fear that I have for most companies when they get into it is you get too big, it can be very problematic. If you're too small, it's pretty problematic as well because you really can't grow out of that little rat race that you're stuck in. So I think it's good to, to find other things to do to be able to, you know, keep that money coming in, keep the, the bank account looking good, keep the bills paid because you're sunk otherwise.

Pete: I witnessed this firsthand. I worked with a company out of Florida who was an insurance restoration contractor this was years ago, and it was right after some hurricanes, and they had more work than they knew what to do with, so they grew exponentially fast,

adding tons of people, running crews everywhere. When we started working with them, there was so much money just flowing all over the place that they had no idea what was even going on in the business. Like, talking with the owner of the company, half the time he didn't even know where money was, who owed him money, what money was still in flux.

Nic: A customer bar.

Pete: It is. Which, to, to your point, the owner was driving, like, a Ferrari. Living large and, and the company looked from the surface level like it was booming. Like, it was just an amazing company that was running all over the state and doing all this work.

But in reality when you got behind the curtain, it was, like, a disaster, right? You've got 40, 50 employees. You've got millions of dollars in flux floating all over the place. No one's really sure where ... what's going on with it. And they ended up crashing and burning because it just was impossible to keep up with.

Chuck: I was in distribution for 15 years before I got into the contracting side, and I'll tell you, as a branch manager of a roofing supply company, you see a lot of things.

I was in Charlotte, North Carolina. We had a major hail storm. It was the largest one in 30 years. Literally overnight we went from one facility to five.

I had to hire a bunch of drivers. We went and bought trucks. We were stockpiling materials left and right, and it was the same thing. Even 15 years ago, it was the guys who were the big shots that were coming in and it's like, "Dude, we just signed a hotel. We just signed this, you know, on Bridge."

And you see them start to kinda slowly fade away to the point where then they're, they're desperate. And I would have guys literally calling me. Chuck, if you don't front me another $40,000 for this next job, I'm gonna go out of business and I'm not gonna be able to pay you any of the other money that I owe you."

Well, dude, where do I sign, right? And it's like, that's how dire it is. Like, you're literally to the point where you have to beg and threaten, but I know you don't have the money. Yeah. And there's nothing that I can do to help you in that case, and I'm sorry, but I also know that you have a drug problem.

I know you're driving a brand new car. You just took your family on vacation. You just bought a new house and this was the best summer of your entire life. Now you're, you're broke and you're pretty much probably gonna be going to jail. So- ... but like I say to anybody that listens, just be very careful about that.

I have a partner in Rio Blanco who takes care of our financial stuff, who's good with money, because I'm not, and I'm well aware of that. You know? Like- ... we're going to Topgolf if we get a, a, a check, you know? We're going to do something like that. So I have to kinda safeguard myself from it as well, and I know that that's just human nature, you know?

Nic: It's funny too, 'cause I see that all the time from the Roofr side.

People's processes, you see how they break down and, and you can normally tell within the first five minutes, I would say, of talking to someone, like exactly where they're going to be and where they're going.

And some people have that mindset, like you're saying, Chuck, where it's just like, "Hey, I gotta take care of the money. I have processes that I need to do and check all those boxes." But when we're talking about using something like Roofr, especially whether it's in insurance or retail side of things, those people who are getting too big for their britches and be like, "I'm gonna do this, and in six months I'm gonna go and open up another location, and I'm gonna chase this storm and build that stuff out," and you're just sitting there and you're like, "Can I offer some perspective?

Can I offer some advice? I don't care if you go with Roofr, but you gotta watch out what you're doing here, 'cause we've seen way too many fail." And that's a reason why, number one, this industry has one of the most amount of money that you can make without having a degree or without having a certified trade red seal or anything like that.

And then also at the same time the trade one of the businesses that can fail the quickest. It's us and, and restaurants that are typically at the highest closure rate within the first two years and first five years. You're looking at within the first two years a closure rate around 87%, in the first five year around 92.

That is a crazy amount because there's a lot of money coming in. It's very easy to get distracted by that shiny object and go after it. And what I think is really great to see, Chuck, is like what you're doing, running insurance for so long, realizing, seeing some of the writing on the wall, and figuring out, "Okay, the next thing I gotta do is I gotta pivot a little bit.

I gotta start taking on retail work, bringing stuff in." And we saw that in another heavy insurance market with another one of our friends at Roofr, with Corey doing almost all retail in a heavy insurance market in Tampa. It can be done. I'm curious from you, what did you see that made you make that pivot?

What was the retail aspect thing that you were like, "You know what? I see all this stuff happening on the insurance end. Let me go and try my hand at retail."

Pete: Funny, I was literally about to ask you the same question.

Chuck: It was years in the making, Nic, and it was like, I'm watching this continue to change as we go forward, and the entire time I've always thought to myself, when I was working retail and insurance, I always liked the retail aspect better because it seemed like, more skill was required. You had to actually kinda know your stuff and be pretty sharp versus, you know, like you said, "Dude, is this even legal?

Like they're signing a blank piece of paper and like basically giving me the rights to everything."

I saw that it was gonna change because you could start to recognize trends. When you started to see claims getting denied more frequently, you started to realize, oh.

And then when your local adjusters started kinda disappearing, and you started getting SeekNow or Ladder Assist or whatever, and it's like, hmm, why is this? And then you start to notice, well, these are starting to get more and more denials. Sure, we can try to fight it or we can do whatever we, we do for you.

I turn mine to a public adjuster 'cause I'm not capable of dealing with that at any level that can actually serve them. So I just did it because I got tired of dealing with all the crap on that side and just realizing that it wasn't gonna get any better.

I don't think it'll ever get back to where it was, but I think that you can go in and you can determine your own value. I've always felt kind of cheap by saying, you know, we'll just do it for whatever they say we're worth, and you don't separate yourself from anybody. You're all just a blank piece of paper at that point, and I always say you might as well put a bag over your head, 'cause who knows what the decision maker's gonna do there, you know?

Free iPads or deductibles or something. But if you actually have to go out there and you have to show your value and you have to explain why you're the best option and separate from the pack, man, that's exciting for one, and if you're good at it, it's pretty, pretty good success rate. So that was my thought process.

I've studied retail sales my entire life and I'm pretty good at retail, so let's just go do retail,

Pete: yeah, and we still see so many people, Nic, that come in and are still just, like, working off of the scope of work and they're just kind of, like, rolling with it. Talk a little bit about, Chuck, how much money is being left on the table by taking that approach.

Chuck: Well, There is a lot, but how do you really even determine it if you really don't know what your numbers are? And so for us, what we do, thank you to Roofr, by the way. You guys are awesome. I have a full proposal ready to go before we even get there. All I have to do is make a couple field checks, make sure the measurements are good, make sure that everything looks right, double check the pitch, get some pipe boots and whatnot, and we can have something together for you right then.

That's got my margins on it that we need in order for Rio Blanco Roofing to not only be profitable, but to continue to scale and grow into the future. Whatever the insurance pays at that point, I could not care any less, and I tell my homeowners, look, if they pay for 100% of it, if they pay for 80% of it, if they pay for, you know, 50%, whatever it is, this is our number, and my approach on that is basically adjusters, I don't know what their experience levels are.

I don't know that this is gonna have everything on it that it should have. In most cases it doesn't, and you have to go through a supplement process. You have to do all this stuff. I put everything on there and then I say, "This is our number. If something's messed up on here, you're not getting a change order.

I'm not doing a supplement 'cause I'm giving you my deal." But it holds me accountable And I just, you know, I've sold both ways. I like the retail model. I like going to people and saying, "Here it is." And it's been very successful because I think we're now at a time where social media and everything being what it is, people are kind of getting a little bit skeptical of door knockers now.

I look on these social media apps. Nextdoor. "Such and Such Roofing is knocking in my neighborhood. What the hell do they want? I didn't call them," you know, "This is annoying." And to me it's like, eh, I've helped enough homeowners here in San Antonio that have been ghosted by other companies after being encouraged to file a claim at the door and then saying, "Oh, you're only getting four grand for your $20,000 roof.

We're out of here." So I don't like to take that approach at all, and that's kind of a long-winded answer, but, that's why I like retail much better and that's why I decided to go that way. It's swimming upstream, but if you're a strong swimmer you still continue to make headway.

Nic: Yeah. It flexes your sales skills.

As someone who's been selling most of his life and building that, like I, I think it's really good to kind of push it. And it's not to say that- Doing restoration work is not sales skills, but it's more like you're a de facto lawyer. You're going through the claim, you're- Mm,

Chuck: yeah. It's a different set of skills completely.

Nic: Yeah. And if you wanna like sell, sell, you're going to go to retail. If you wanna be like a claims advisor and stuff like that, then that's the insurance side. When you were doing that transition there, do you have any tips for having people... I know you said knowing your numbers is important so shout out to Roofr and, and the proposals.

But what are some other tips that you have for someone who's looking to transition a little bit more into retail or make that jump entirely from insurance?

Chuck: Well, I mean, for me it's been kinda awesome because a lot of our retail deals have actually been insurance claims that we flip to retail. So we're still getting paid at the end of the job, and then it's like, "Okay, we'll send you the paid in full invoice.

You can send it to your insurance company. They'll reimburse you much quicker than they'll reimburse us if we call them every day begging for our money." And it's been working out well because we found our perfect client for that. Property owners, property managers, people that have multiple roofs that they've got to get taken care of.

And we have one guy in Texas here that we've done like 14 roofs for, and it's all been the same way. We gave him the retail number. Every single one of them has worked out just about identical to where the insurance was, 'cause we do know our numbers and we're not thousands of dollars off by any means.

And it's, it's worked out. They pay it and at the end when the check clears, we'll send you the paid in full, you take care of it and move on to the next. And we've done that with several homeowners. We offer financing options, but haven't even had to use that thus far because, you know, like I said, we've dialed in who our ideal client is, and our ideal client just happens to have the money to be able to front that and then get paid from the insurance on the back end.

It's helped us elevate to a different level as far as the projects that we're doing, because we can turn down some of the smaller ones that we normally would be doing just for insurance money and say, you know, "Hey, if we're too expensive or whatever, that's cool.

We appreciate the opportunity, but have a great day." And we just continue to seek out our ideal clients.

Pete: I remember talking to a contractor maybe, like, about a year ago or so kind of about this similar topic, and he kind of went the same direction you did. He just now treats everything as retail.

Okay. And one of the things that he said specifically that stood out to me was he said, when we really dialed down our retail proposal, we end up very close to the insurance number anyway." And he said, "Because we're so close or sometimes even right under," he said, "We get bought off by insurance 99% of the time."

He's like, "They don't even question it." He's like, "It's, we used to fight like crazy for every dollar with them," and he's like, "Now that we present these retail quotes that are very, very similar to what they're at with their scope," he's like, "We get almost no blow back at all from the insurance company.

They just approve it on the spot." He's like, "It's been way easier to get approved, honestly, since going to a retail first model."

Chuck: I think so too. As long as you know how to do it and you've got everything factored in that you're gonna need, it's good, it's no different than saying, "Hey, you don't have enough pipe boots on there.

You don't have this. We're gonna have to supplement it, but here's my front end deal. I'm willing to accept this, and I don't even care to supplement it because I know it's right."

Nic: Mm-hmm.

Chuck: And you're spot on. They're like, "Okay, cool. Let's do that." Maybe you're like 30 or 40 bucks less than what they would've paid, and they're, like, high-fiving each other

Pete: Yeah.

Chuck: they got one over on the contractor. But at the end of the day, we're still getting it, and I think that the homeowners are very receptive to that as well, and they notice. I don't have that animus, like, "Let's go fight the insurance. Screw them," you know, like us against them. I think we all are trying to work towards a common goal.

The homeowners, the carriers, the contractors, we all want the same thing. It's just, sometimes the representatives from each, each individual party there can maybe speak on behalf of others that they shouldn't be.

But I think at the end of the day, we're all trying to work towards the same thing. And I've done that same deal, and it's been... been flawless, my friend. No problems.

Pete: Well, and I think one thing that's not touched on enough in this whole thing, Chuck, and maybe you can speak to it here, is the customer experience side of it, right?

The difference in the experience for a customer when they're doing it the way you guys are doing it now versus how you guys were doing it when you were totally insurance based, and what is the differences for a customer?

Chuck: Well, it's night and day because you can really give them that five-star experience, you know?

We're gonna change out all the flashing. We're gonna tear off all the roof. We're not gonna leave three or four layers like we find all day over here in San Antonio. We're gonna do it right because th- we're putting our name on this. We're putting our reputation. This is 100% us.

We're putting a warranty that's gonna be there for life. We're putting general maintenance on your roof. We're qualified to offer a $25,000 guarantee from an outside source because of our quality, right? And that costs money. That's not cheap. That's not free. If you're doing the insurance work, I mean, dude, I've seen insurance scopes where they claim that they're not gonna pay for drip edge on the eaves because it wasn't directly hit by hail.

So what are you supposed to do, if it was installed correctly, you technically shouldn't have to take it off, I guess, but how many people install it correctly? Not too many. Just the little shortcut stuff like that that you kinda have to get forced into, and that's why I always tell people, you know, on the insurance side it's a different contract, it's a different everything, and it basically says, you know, we're doing exactly what they say to do.

We know that that's maybe not the very best situation, but we're doing what they say. Chimney flashing, I guess in some people's opinion, is ice and water shield around the base of the chimney. And we do chimney flashing, you know? And it costs more than what they pay for that on the claim. So the experience is always better, and I can tell you right now, I went to help one of my clients from, eh, about four years ago yesterday.

She got an email from me through Roofr that said, "Hey, give us a call. It's time for your roof checkup after three years." I went out to her house, and before I even got out of the car she's running out there smiling, "Hey, Chuck, good to see you." And that was a cash deal, you know?

We made her feel important. We took care of her. It wasn't just a transaction. It was an important meeting with us, and when she needs us, we're there for her. And to me, that's the difference between one and the other. If you come into town, you knock out 300 or 400 roofs- how can you maintain that same level of personal experience, personal touch with the homeowners?

You can't, and your quality suffers as well, yeah. Since we've lowered the number of jobs and, and higher the margins, we don't get callbacks for leaks. It's awesome. Like, whenever it rains, I just kinda go, "Oh, man, this is beautiful. It's raining out," and nobody calls yelling about anything.

Nic: When you talk about the, that customer experience and yeah- Yeah ... like being able to spend that time with them, going through everything that's in there, explaining the difference between what an insurance scope is looking like in there, and where, "Hey, you're gonna pay a little bit extra for this, but this is gonna go a long way.

It's gonna help you up. We'll do three of your checkups with you. We'll send you emails. You don't have to think about it." That's one thing, but I also think about the other side of things when we're talking about the rise of retail and have it coming in. There is across the country and in Canada, we're seeing insurance companies send those homeowners those letters saying, "Hey, your roof is 15 years old.

And if you have that organic asphalt shingle, then that's in timeline. But there's also times in which you're getting that letter when you have that fiberglass architectural shingle, which should be lasting that 40 to 50 years, at that same timeframe, at 15 years. Are you gonna go fight the insurance company, or are you gonna provide them with value on repairs and inspections, everything else?

And that opens up the door to a way better response rate, and I'm going to assume, Chuck, and my question to you is the referrals that you get from there. You mentioned you keep on talking to customers that you've worked with in the past. I'm sure the insurance aspect has helped, but the retail aspect is pushing it out across the board even more.

Chuck: Oh, yeah. And that's just my thing, you know? I love to thank my, my homeowners for their business. We wouldn't be here without them. It's so crucial to me to remember as many people as I can, I remember my very first customer here in San Antonio. It was crazy.

He calls me up and he says, "Oh, yeah, you know, my name's yada, yada. You did my roof five years ago." And I'm like, "Oh, yeah, you know, thank you for your service to our country."

Or, "How's your dog doing today, Lily?" I sold a roof one time because I remembered the name of the dog. And the only reason I remember the name of the dog is 'cause my dog's name was Lily as well. So, like a year later I sent him a letter and I was just like, "Mr.

and Mrs. Yada Yada and Lily, I hope y'all are doing well. I just wanted to make sure that you were able to take care of the roofing needs." Dude, that week I signed that roof replacement form because that was just a personal thing.

That's the most important part of it for me, because we are referral based and, people are gonna give you referrals if you remember the name of their dog or you, give them a little bit of grief because the Texas Longhorns can't beat the Ohio State Buckeyes or whatever.

But just stuff like that, and you have a good time with it, and you, you make that an enjoyable experience, you know? Buying a roof sucks. Nobody looks forward to it. So our biggest responsibility is to at least do our best to make it fun.

Pete: And I remember one of the points that was made here when we had the hailstorm was the local guy saying, you know, "Hey, if you hire this guy from out of state, what do you think is gonna happen if that job he does leak when it rains?" Right? Do you think he's coming back from three states away to fix your roof?

Probably not, he said, "And I'm not going to come and patch his work." So now you're in this weird situation, right? Using that local guy that's probably your retail guy maybe makes more sense in the long run altogether as a homeowner, right?

Chuck: I think it does. And I mean, I've gone and worked in major hail markets.

Amarillo, Texas years ago. And there's like two local roofing companies that have been there for like 40 or 50 years, and everybody in town used those two. So I was like, all right, you know, I gotta get out of here because I'm gonna starve. But I, I kind of appreciate that as well. When I was in College Station, they would literally go on the news and be like, you know, "Just shop local.

These storm chasers, they suck. They're gonna come in, they're gonna ruin everything." And some of the biggest companies in the United States would come in there and they'd be gone in like a week.

Pete: I mean, I saw it firsthand. They literally ostracized people that were from, like, literally the next town over. "I shop in your town. How can I not get a, a deal? I can't even get at somebody's kitchen table," right? And they're like, "I'm practically local," and they're like, "Nope."

It was funny to watch. But we got a couple questions here I wanna just throw out there to you, Chuck. The first one I saw was Ted asking, "If a homeowner is doing retail on an insurance claim," or I guess insurance on a retail job, right?

Like, "how do you advise them to collect on the depreciation?"

Chuck: We literally just sit down with them and say, "Okay, this is gonna be the cost to do the roof. If it matches that, great. If it doesn't, great." And like I said, we have really honed in on who our ideal clients are.

So we don't have a lot of people that are like, "Oh my gosh, you know, I don't have that $3,500. I can't give it to you until it comes." Most of the people are happy to do it, so we just say, "Look, you pay for the roof. This is our price. We'll send you the paid in full invoice." You may get a little bit less or whatever, but that's basically how we do it and completely stay out of the process. And, it seems like it works well for the homeowners. They get paid a lot quicker back the depreciation. They're a lot more motivated to care about the depreciation.

You know? Once the roof is on and the check that's being, it's gonna be here today or tomorrow, it's for the roofer. They don't really care that much. So once that roof's done, you're kind of on your own as far as trying to collect that last check, and this definitely eliminates that from being an issue because homeowner cuts a check, they're immediately like, "Bro, where's my money at?"

And that money usually comes back within a day or so. So it's worked out well for the homeowners, but we've just literally on the front end just said, "This is how we're gonna do it."

Nic: Also, you take out that red tape of having to converse with the insurance company. 'Cause they're just gonna say, "We're gonna talk to the policy holder and that's it."

Yeah." And they can just push back, and you're putting more friction in the wheels there. So as long as you can kinda open it up, I can see, to your point, how that could be a lot easier for that homeowner to get paid quickly.

Also, not having to supplement and ranking up that bill as much as you can, that's gonna allow them to get paid quicker too, 'cause the insurance was like, "Yeah, yeah. We said 10,000, here's 10,000. There you go." Yeah.

Chuck: Everybody wins and everybody's happy.

Nic: Not always it's gonna be that easy, but the majority of the times it is.

You're gonna get a claim adjuster here and there that's a little funky.

Chuck: Oh, absolutely. I mean, that's the nature of the beast, you know? I love adjusters, but you know, not every single one of them.

Nic: yeah.

Chuck: Everybody's got problems, so I can respect it. But yeah, it's a lot less stress.

We don't have to go out there and we don't have to meet the adjuster. We don't have to do any of that stuff. If you get this back and it looks bogus to you, you know, we can, we can send you to our public adjuster or we have a supplement company that I'd be happy to send this over and have them look at it. If it's grossly undervalued, if it's $10,000 less than what we think.

But like you guys said earlier, we're usually within a few hundred bucks, give or take. It's been pretty simple, you know? When you show someone the number on the front end and then you say, "I don't even wanna see your insurance paperwork. This is how much it is," and then they look and say, "Well, yours is only, like, $400 different."

Yeah, cool. I know what I'm doing. Ask everybody else if they can do the same thing and see where their numbers are.

Maybe they don't know what their numbers are. Maybe they're literally just flying blind, and that's a good way to capitalize on some opportunities as well.

Nic: That's a great point with knowing the numbers.

Chuck: If, if they're close, they're close, right? I mean-

Nic: Yeah

Chuck: I've never had a homeowner say, "Yours is ridiculous compared to the insurance." It's usually within 4 or 500 bucks one way or the other.

Pete: Well, and I love the fact that you're not waiting on their paperwork either, right? Like you said, "I don't even wanna see it," right? It has nothing to do with me.

You know, here's my number. That's all I care about, right? Yeah. That's a completely different approach. It works to your advantage 'cause it makes you look much more confident in what you're doing, in your numbers and, more experienced, obviously.

Better street cred, right?

Chuck: And it's crazy 'cause for years I sold the exact opposite of that, you know? And it was like, "Well, we're gonna go off of what the insurance says, and if it's not right, then we can supplement it. We can do this." So there's no right answer or wrong answer. Mine was 100% based on cashflow and also just the fact that I just got sick of dealing with it, there's success to be made on either side if you do it the right way. It's just this way is a lot less stressful.

Pete: We got another question here about your marketing and advertising Chuck. Says, how is it directed at, as retail?

Chuck: It's really not, to be honest. I mean, we don't literally say, you know, "Hey, we're 100% retail based company."

Any opportunity you can get in front of a homeowner is gonna be valuable. The right customers are always gonna be there if you make yourself available to them. I certainly don't go out and say, you know, we're insurance specialists or we'll do the job for your deductible. I don't advertise any of that stuff.

There's plenty of that going around in the world, and I just feel like you kinda lose yourself there in a sea of sameness. So I don't really advertise it as a retail company. We advertise it as, you know, we offer payment options, we offer premium roof systems, we offer alternatives to, replacements.

We're experts at chimney flashing. My guy Francisco goes out and builds a amazing piece in someone's yard, puts it up there, and then we say, "Okay, that's 1,200 bucks." We collect on it and everybody moves on.

So it's not bad. You just have to set the expectations with the people and tell them, "This is how much you're gonna pay, this is when you're gonna pay it, and this is what you're gonna get."

Pete: What would you think, Chuck, would be your biggest pieces of advice if I'm someone who maybe traditionally was in your shoes, right? Someone who maybe got into this because of the insurance side of the business. I've been working in insurance. Obviously, I'm seeing, you know, some issues there, and I'm thinking of making that move to retail.

What would be your biggest advice to that person?

Chuck: Just do it. I mean, that's literally the only thing. You just have to do it. Jumping into retail, I knew it wasn't gonna be super easy, and it's not super easy.

And the opportunities are fewer than they are if you're willing to just go out there and do whatever for whatever. So building that up is something that if you're gonna do it, you just gotta start. And you have to be willing to accept the fact that you may still have to eat a little bit of that insurance stuff moving forward just to kinda keep money coming in.

But once you hit that point where it's working for you it's great. You just continue to develop the machine as you go and, build to the sky. That's really the mindset behind the retail is just scalability, long-term sustainability.

And, you know, unfortunately, I just think that model that we've been used to for all these years that made us all this money and gave us all the opportunities that it did, 'cause the insurance market's been great to me. It's just, I feel like it, it got too big. So now's the time to jump off and try to separate yourself from the pack, right?

Nic: So it kinda ... Yeah.

Chuck: I just wanted a graphic. That was all I was trying for there.

Nic: Oh, Joel's got graphics. Don't worry.

It kinda leads to one of the other questions that we had there, and, I think I, I know your feelings on it, but might as well give it a go. But do you think that there's a time that insurance is gonna come back?

Chuck: I guess it kinda depends on your definition of comeback.

Nic: Mm-hmm.

Chuck: Do I think we're gonna come back to the point where you get the local adjusters that are at the yard and you say, "Hey, Tony. How's it going?" And you and Tony go up there and he looks at your stuff and says, "Yeah, you know what? That's great." I don't think so.

I think they kinda realized that model was maybe bleeding a little more money than they would've liked. I think it's easier now to deny claims when you don't have a physical representation on the site. When someone knocks and says, "I'm just a messenger. Please don't shoot me," I think that probably appeals to them, you know?

And so I don't think that's probably ever gonna come back to being the way it was then. Do I think it's gonna come back in some degree? Yeah, of course. I mean, insurance is never gonna die. It's always gonna be there. As long as mortgage companies are involved, I mean, there's no way it can die.

They're all tied together, you know? But it's like, what are you gonna do in the meantime? You've got to figure out how to survive this little lapse in history where it's gonna change, and I do think it'll come back. I think that after several years of ineptitude, or I think the MRP programs have proven in the past that sometimes they work to great scale, sometimes they fail at a great scale.

The quality of workmanship that we're gonna be seeing versus the money that's gonna be available to the actual contractors it's gonna suck for a while. So it'll come back, but I think a lot of people that are in it right now will probably not be at that point, and that's probably why it's gonna come back, quite frankly.

Pete: Do you think in the future it's gonna be more the retail guy doing the insurance work that's in his region backyard versus the guy who's driving three states over chasing a storm?

Chuck: I do think it's gonna be a lot easier to be the retail guy at this point that's, you know, stays local. I think storm chasing has kind of gotten a bad rep. You know, there's a lot of national news and a lot of people that get ripped off, and you can't help but see that stuff. So I do think that that's gonna be, the better option.

I think staying local. The communities that have been doing that for decades already they've never had any problems. I never saw anybody in College Station, Texas talking about, "My grandma got ripped off. Someone stole her deductible," 'cause they kind of policed it themselves.

Maybe we can get back to a better picture of what it should be. And instead of being so contentious it can be fun again. We can all get along. Adjusters and roofers and homeowners can sit out on the porch and smile and laugh after the job's done, knowing that everybody was taken care of and it was right.

Pete: We got a question here: Do you even bother to meet with the insurance adjuster on site?

Chuck: I tell my homeowners, "If you would like for me to be there to provide peace of mind to you, I'll be there." But the reality is I'm just gonna stand there and watch some dude take pictures most likely, and if it is an actual adjuster, I am not gonna sit here and argue and I'm not gonna get in a fight in your front yard.

I'm just not that guy. I'll be very cooperative. I'll offer to let him use my ladder. You can use my chalk. You can do whatever. I guess I'll always do that just as kind of a, a way to make my homeowners feel happy, to make them feel more confident or comfortable that they're not getting screwed, even though I tell them straight up, you know, "You're probably gonna get screwed even if I'm standing here.

There's nothing I can do about it. But, I'll make sure he takes all the pictures rather than taking them at some weird angles or something and I'll at least fight for you on that front." But at this point, it's not even really adjusters anymore, so it's kinda... It's pointless really, unless you're just doing it as a dog and pony type thing, and that's, you know, that's just my honest opinion on that.

Pete: Yeah. Rafael's got a question here about private equity. Do you think private equity will start to affect the retail market more, or do you think they'll stay on the insurance side more?

Chuck: I think they're designed for the insurance side, honestly, and I believe that that's exactly where they're gonna stay.

I think these big organizations and conglomerates are literally being built right now for the purpose of serving as manage repair programs or, preferred contractors for the insurance carrier. So I don't see them coming into retail. I don't see there being any point to that. I think that they're specifically designed for that purpose and, maybe I'm gonna be wrong, but I don't think so.

I don't see there being any, massive private equity companies going into, commercial roof coatings or something like that. It's gonna be pretty specific to what they're doing, and I'm cool with that. And there's gonna be a lot of people that jump on board and a lot of people that jump off, and it just kinda is what it is, but I don't think they're gonna ever really affect retail that much.

I don't think they have the ability, honestly. I think it's scaled more for massive amounts of volume and nothing more.

Nic: There's way too many nuances and process updates in the retail framework that's so vastly different per market, and per inside that market, there's different regions, right?

Whereas insurance is like, yeah, it changes state to state, but you can pretty much get by if you're running the same insurance numbers. You can get it across the board. So it's, it's a much easier packing repeat type system than it is for, retail.

Chuck: Absolutely. I just got the memo, guys. We are out of time.

We have- ... basically blown through that hour. That was awesome. I appreciate that very much.

Pete: Let's spin that wheel, y'all.

Chuck: Got William McLean.

Pete: William.

Nice. Save that Carhartt hoodie for a rainy day. Little hard- Those Carhartt hoodies are

Chuck: awesome, by the way.

Nic: I, like, every Carhartt thing. Joel, call Richy. Pete and I want Carhartt shit.

Chuck: I wrote it into my contract for the Keeping it Real show, so, like- ... I literally am like, "Y'all gotta send me some socks and stuff." So they're really good about sending me socks and hats. I got some of the greatest Roofr apparel on earth.

It was an honor to represent Roofr that month, February this year, as the Roofr of the Month, and I appreciate everything you guys do for us. Y'all are absolutely some of my best buddies in this industry and I absolutely love this.

Pete: Well, thank you for jumping on, Chuck. This has been great. I think a lot of good insight, into it. Some stuff to think about if, you know, some people listening are maybe on the fence here as to how to proceed into the future. Or maybe looking to move on from insurance.

I think there's some great insight on how you guys did it and how you guys are handling it. So thank you, man. I appreciate you jumping on.

Chuck: Anytime.

Pete: All right. Well, thank you everybody for joining us, and we will see you next time on the Roofr Masterclass.

Nic: Thanks, everyone.

Latest Masterclass

How to Get Commercial Roofing Jobs (with Bryan Mitchell)

Commercial roofing expert with 40+ years of experience, Bryan Mitchell, returns to share how to find, win, and succeed at commercial roofing work.

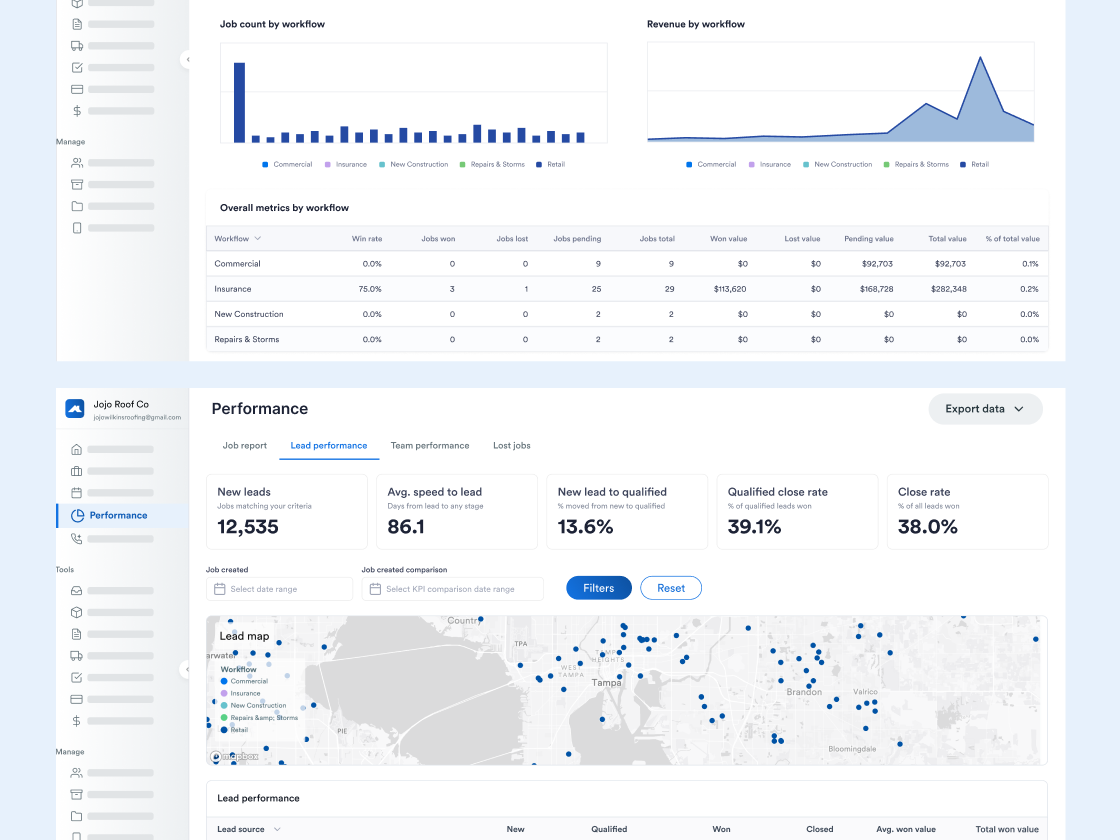

Unlock the Matrix with Performance Dashboards

Your whole roofing business lives in Roofr. Now, your reporting does too — and if you’re not sure how to best leverage it, let us show you how.

Customizing Your CRM to Match How You Do Business (Roofr Plans Explained)

Hosts Pete and Nic help four VERY REAL guest roofers find the right plan for their needs. Tune in if you could use a chuckle and want to learn more about Roofr.